The financial services industry is going through changes. Tech is evolving fast, and customer expectations are higher than ever. It’s exciting, but let’s be honest, it can feel a bit overwhelming, right?

This puts the banking industry in a tough spot. Banks need to change how they operate to keep their current customers happy and attract new ones. That’s why we’re seeing such a big push for digital transformation. It’s all about focusing on the customer and staying relevant in the banking sector.

In capital markets, fintech companies are stepping up, solving problems that traditional banks have struggled with for years, like outdated systems and clunky processes. The speed of change in the industry is driven by ultimate banking technology trends like AI, virtual assistants, and better security.

Futurist Brett King has already hinted at what’s coming: a future with banking without banks. Imagine billions of people accessing financial services daily without the need to visit a bank.

“By 2030, I would say that you probably have two billion people that’ll be using day-to-day banking services, independent of banks.”

(Brett King, Australian futurist)

What’s next for the banking industry in 2026? What innovations will reshape both traditional banks and fintech companies? Let’s dive into the ultimate banking trends.

Traditional Banking vs. Digital Banking

Before diving into ultimate banking trends, let’s differentiate between traditional and digital banks to understand their pros and cons within the banking industry.

Traditional banks are the banks you’re probably familiar with. They have physical locations where you can walk in and talk to someone face-to-face. For example, JPMorgan Chase and Bank of America fall into this category.

Why people opt for traditional banking

- In-person service: Need to talk to someone to answer your questions? Just visit a branch. 38% of customers still consider physical branches essential.

- More products: Traditional banks often offer many services like loans, credit cards, and investment advice.

- ATM access: They usually have a large network of ATMs, making it easy to get cash.

Downsides of traditional banking:

- Higher fees: You might pay more for services like account maintenance.

- Lower interest rates: Savings accounts often have very low interest, around 0.01% – 0.02% APY.

- Documentation: Sometimes, opening an account requires more paperwork.

Online banks exist entirely online, offering services through websites and mobile apps. They don’t have physical branches.

Why people choose online banks

- Higher interest rates: Savings accounts often offer much better rates, typically between 4.00% and 5.10% APY.

- Lower fees: Without the costs of maintaining branches, online banks can offer lower fees.

- Convenience: You can bank from anywhere, anytime. That’s why 78% of U.S. adults prefer to bank via a mobile app or website.

Downsides of online banking:

- Cash deposits: It can be tricky to deposit cash since there are no branches.

- Limited services: Some online banks might not offer as many products or services as traditional banks.

So, both types of banking have their pros and cons, which is why people choose between them. However, online banks are gaining popularity over traditional banks, highlighting the importance of the rapidly evolving digital landscape.

Ready to elevate your online banking? Contact us to create secure, user-friendly solutions tailored to your needs!

Digital Banking Landscape in 2026

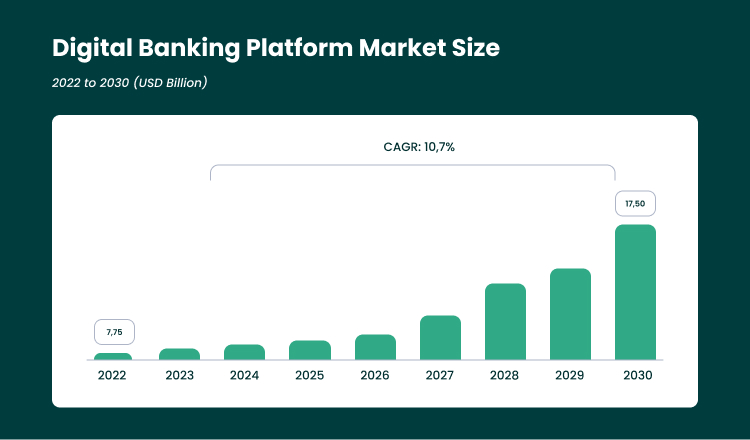

According to the Vantage Market Report, the global digital banking platform market was valued at $7,75 billion, projected to reach $17,50 billion by 2030. Plus, the annual growth rate can reach over 10%. Sounds promising, but what has contributed to this sudden growth of the banking industry?

The main factors fueling the growth of the financial services industry and the emergence of ultimate banking trends are digitalization, technological advances, and customer-centric financial solutions.

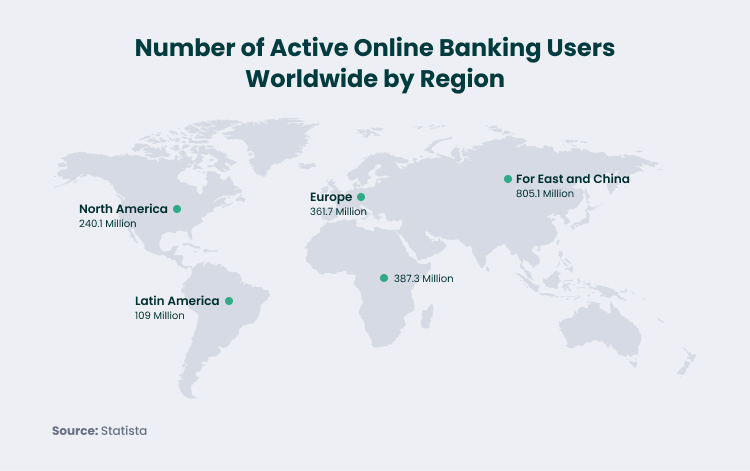

When talking about country segmentation in capital markets, Asia has the largest number of online banking users, 805,1 million. When it comes to market share, North America occupies a leading place with 37, 3% and a net worth of $2,9 billion. But Europe is also a region where online banking businesses prosper.

Most banks now have a solid level of digital maturity, shifting the focus to ongoing transformation. Over 53% of banking leaders are actively working to enhance their digital efforts.

Currently, 35% of global banking executives are pushing forward with digital initiatives. But 12% are still in the planning phase, and 6% have no immediate plans to act. Only 1% of banking leaders are uninterested in digital transformation, a drop from 6% last year.

Digital banking is becoming the norm, with 77% of Canadians, 71% of Americans, and 69% of Spaniards using online banking monthly. Traditional banks must invest in full digital transformation to keep up with these expectations.

Transforming a bank isn’t easy. It’s a slow, complex process requiring a deep understanding of customer data, mostly their needs and priorities. Success depends on the approaches and trends in digital banking you tend to adopt to digitalize your financial operations.

That’s why we’ve prepared a list of top digital trends in banking for the upcoming year to simplify digitalization for your business.

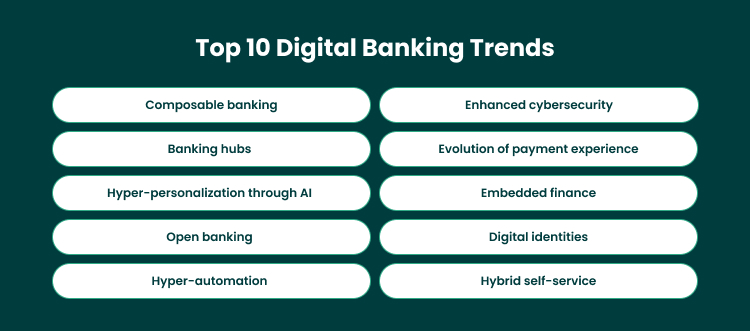

Top 10 Ultimate Banking Trends for the Upcoming Year

The traditionally stable banking industry can’t afford to stay still. This has paved the way for exciting innovations and transformations.

First, cloud and AI technologies are pushing banks to adopt cutting-edge solutions. Second, customers now expect hyper-personalized services, real-time insights, and smarter, data-driven decisions. Lastly, fierce competition from fintech and big tech is driving financial institutions to innovate like never before.

Let’s dive into ultimate banking technology trends for 2026 that will shape the financial industry and help banks stay competitive in this fast-paced landscape.

Composable banking

Composable banking is a top banking trend that helps banks stay competitive in the financial services industry. It’s all about combining multiple existing solutions. Instead of creating everything from scratch, you can plug ready-made platforms into your system, adding the features you need.

This approach allows smaller financial institutions to compete with big banks by providing high-tech solutions and showing operational efficiency. For example, Starling Bank, a UK-based digital bank, is a leader in composable banking. They use a modular, API-driven setup to offer flexible, personalized banking services tailored to their customers’ needs.

Banking hubs

Banking hubs are shared spaces, similar to a regular bank branch, but open to everyone. Run by Post Office employees, they allow customers from any bank to withdraw and deposit cash, open bank accounts, pay bills, and handle everyday banking tasks – all in one place. This saves time and makes banking more accessible to everyone in the community.

This ultimate banking trend is growing, especially in areas where traditional branches have closed. For example, Britain already has 76 banking hubs, with plans by LINK and Cash Access UK to increase that number to 100, ensuring essential financial services remain available.

Hyper-personalization of banking through AI

Artificial intelligence is a digital banking trend that has firmly taken root in financial institutions. AI is transforming the banking sector by delivering hyper-personalized experiences to customers. The era of generic financial advice is over. Now, AI enables banks to offer services uniquely tailored to each individual’s needs.

By analyzing your data, AI predicts what you might need next, like a new savings plan or investment opportunity. It can also suggest smart financial moves, such as when to refinance a loan or invest in stocks. With AI implementation, banking becomes smarter, more personal, and perfectly aligned with your financial needs.

For example, JP Morgan Chase uses AI to speed up loan approvals by analyzing your credit history and transactions, offering personalized loan options quickly and efficiently.

Open banking

Powered by APIs, open banking is shaking up the financial world by allowing third-party developers to build new apps and services around banks. This ultimate banking trend is all about collaboration, especially between traditional banks and non-banking financial companies. It means more personalized financial services, better tools to manage money, and often better rates thanks to increased competition.

Take BBVA, for example. They’ve opened up their banking platform to outside developers, letting them create new financial services using BBVA’s APIs. This kind of teamwork is reshaping online banking, benefiting everyone involved.

Hyper-automation and robotization

RPA, or Robotic Process Automation, is another ultimate digital trend in banking. It uses software robots or “bots” to handle repetitive tasks like data entry and compliance reporting, making operations faster and more efficient. Recently, RPA has even started to tackle complex processes like mortgage processing.

Around 53% of organizations already use RPA, and another 19% plan to start soon. About 80% of leaders in banks are adopting RPA or plan to. The goal is to automate routine tasks, so banks can focus on more important work. For example, DBS Bank uses hyper-automation to speed up customer onboarding and quickly verify customer information.

Enhanced cybersecurity

Focusing on cybersecurity is another banking trend today. With technological innovation, banks deal with the dilemma of how to spot and stop fraud while keeping financial operations running smoothly. That’s why banks opt for AI-powered fraud detection systems to identify suspicious activity in real time.

These AI systems don’t just detect threats, they can prevent them too. With AI in cybersecurity and automation working together, banks can ensure their operations stay secure and reliable.

For example, Wells Fargo uses advanced AI and machine learning algorithms to monitor and analyze customer transactions. Their system can detect anomalies and potential security threats, ensuring that any suspicious activity is quickly addressed.

Evolution of payment experience

The evolution of payment experience is another ultimate banking trend that changes how clients pay for goods and services, significantly enhancing customer satisfaction.

- Real-time payments: Customers can send money instantly, anytime, day or night. Real-time payments are becoming the go-to method for businesses, making cash flow smoother and cutting down on the hassle of paperwork.

- Digital wallets: They are taking over, especially with young people. Digital wallets are convenient, easy to use, and super popular.

- New payment tech: Contactless payments are now on wearables like smartwatches, making it even easier to tap and go. These types of payments are expected to hit a whopping $10 trillion globally by 2027.

Embedded finance

Embedded finance is transforming banking by integrating financial services directly into non-financial platforms. This ultimate banking trend allows financial organizations to connect with customers through various digital ecosystems, reaching new markets and simplifying customer acquisition. It also makes banking services more accessible and tailored to individual needs.

While many banks are interested in embedded finance, a study by the Boston Consulting Group shows that only 27% of leading banks are fully engaging in these collaborative ecosystems. Most are still in the early or testing phases.

Digital identities

Digital identities for secure authentication are becoming a major trend in the banking industry. They allow people to verify their identity online while keeping personal data private and under control, which plays a crucial role in risk management by reducing fraud and unauthorized access.

In developing countries, digital IDs can drive growth and inclusion. McKinsey estimates that adopting efficient digital ID systems could boost economies by 3 to 6% of GDP by 2030.

Hybrid self-service

Customers expect more from online services. They want to handle things on their own, anytime they choose, with the help of websites or mobile banking apps. But when a digital banking platform doesn’t meet their needs, they still want the option to talk to a real person. This is a challenge for many services, especially those related to asset management.

While AI has improved customer support, chatbots can’t solve everything. For complex issues, especially in banking, people prefer speaking to a human who can offer the emotional support needed, something AI can’t provide.

A recent Deloitte survey found that while customers are fine using AI for simple tasks, they want real humans for more complicated services like mortgages or financial advice. So, hybrid experiences, combining digital and human support, are more effective than purely digital or in-person services.

Challenges Stopping Banks from Digitalization

Even though adopting ultimate banking trends has significant benefits, there are still some factors preventing banks from fully digitalizing, especially in capital markets.

First, bank leaders are hesitant due to cybersecurity concerns. They need to strengthen their defenses against cyber threats that target customer data and transactions.

Second, many banks have legacy systems that are complicated to integrate with new technologies. This process can be time-consuming and expensive and requires careful planning, testing, and smooth integration.

Third, banks operate across various regions with changing laws around AI, data protection, and financial transactions. This leads to uncertainty and the need for banks to adapt quickly.

Despite these challenges, online banking remains full of opportunities, promising higher revenue and more loyal customers.

Facing challenges with your banking solution? Contact Forbytes to streamline the development process and drive success faster.

Final Thoughts

At Forbytes, we’re all about digital transformation. We help businesses adopt the latest banking trends, building user-friendly, efficient solutions that drive revenue growth and boost operational efficiency. We offer financial software development services to help banks, funds, credit unions, trading companies, and other financial institutions modernize, improve performance, and enhance risk management.

We specialize in expanding your software’s functionality, enhancing security, and integrating third-party tools to streamline your operations.

If you’re ready to embrace the future of digital banking, Forbytes is here to help. With our expertise in finance and banking, we can be your trusted partner in turning your ideas into powerful fintech solutions. Reach out today to get started!

Our Engineers

Can Help

Are you ready to discover all benefits of running a business in the digital era?

Our Engineers

Can Help

Are you ready to discover all benefits of running a business in the digital era?