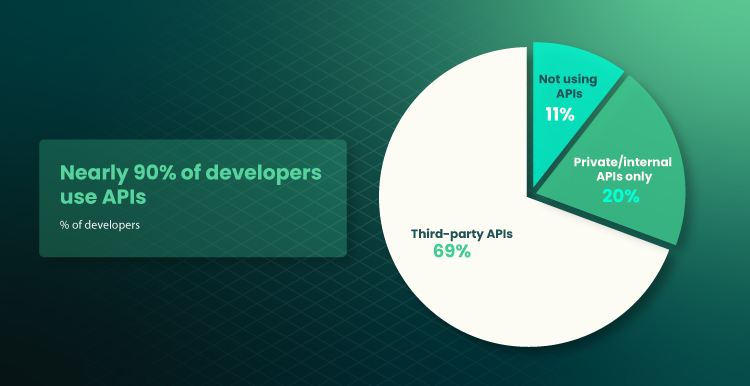

Under the Nordic APIs research based on the SlashData report, about 89% of developers worldwide used Application Programming Interfaces to a varying degree in 2020. The diagram below confirms it. Nay, according to DEVELOPSdigest, more than 98% of entrepreneurs consider this technology a critical part of the digital transformation of their companies. Furthermore, over 68% of developers plan to increase API usage within their projects. And this index includes numerous open banking and finance APIs.

Nowadays, most business owners in developed countries use financial Application Programming Interfaces. However, experts advise implementing such technology only with the help of authoritative IT agencies (for example, forbytes.com). It’s due to the integration of financial APIs requiring specific skills as well as knowledge. Using the services of unchecked specialists may lead to the wrong operation of such interfaces. And it would decrease companies’ income.

Key Open Banking Features

Some experts say that such a technology was initiated in 2018 by the UK Competition and Markets Authority (CMA). The latter ordered banks to open their applications for third parties. But in fact, open banking appeared in 2015. At that time, the EU updated the Payment Services Directive (PSD2) for similar purposes and introduced new security rules for accessing payment accounts and financial transactions.

Both directives allow using open banking API for data aggregation from different bank accounts into a single view provided by a TPP application. It helps third parties to create better PFM (personal finance management) applications. Moreover, such an approach to banking API development pressurizes existing incumbents to improve their services. So, the latter have to either enhance their offerings or cooperate with fintech.

What About the Early Open Banking Projects?

Nowadays, fintech APIs provide customers with high-security protocols. Moreover, PSD2 allows such digital products to collect and complete finance information regardless of changes in the operation of banking applications directly.

And the early open banking projects had numerous cons, namely:

- Couldn’t collect data if a bank changed the algorithm of its application;

- Were too expensive to use;

- Collected data from common sources but didn’t provide comprehensive information for third parties.

Thus, the early projects couldn’t provide the proper level of services to build a complete international API ecosystem.

Main PSD2 Peculiarities

This regulation governs fulfilling payment services within the EEC and the EU. So, the directive combines the API, open banking, and the financial industry ecosystem into one. Thus, third parties can access information about the client’s bank account with the user’s consent.

PSD2 has added two additional roles to the industry landscape. The first is AIS. It’s an online aggregator that collects information from multiple client accounts. The second is PIS, which provides transaction initiation on the user’s behalf as well as funds management.

The regulation took effect in January 2016. Additionally, EBA issued the ultimate version of the Regulatory Technical Standards (RTS) in November 2017. The latter defines the general requirements for the API financial services and the method for implementing the directive. Finally, each EU country had to implement the regulation into local legislation by January 2018.

Are Open Banking APIs Reliable?

To answer this question, customers should first understand what API is. So, it’s a set of protocols and codes that allow software and apps to communicate. Thus, a system can request information or “contact” another one by applying an API. Then, the needed data may be exchanged between the two systems. As mentioned earlier, banking APIs connect licensed third-party providers to a bank in an efficient, standardized, and secure way. So, such digital products are some software bridges.

There’re several types of API fintech:

- Private. They’re used within the systems of certain banks or other financial institutions. As a result, there’s a low probability of hacker attacks or getting infected with malware.

- Partner. Such APIs are often created for business partners of financial institutions. Here’s a higher risk of getting a digital virus.

- Open (or third-party). This type is used for providing an open banking operation.

Of course, the last type of financial services API is at high risk of being hacked or infected with malware. Moreover, problems in such digital interfaces may lead to essential financial losses. That’s why numerous clients and banks are worried about the safety of using such APIs.

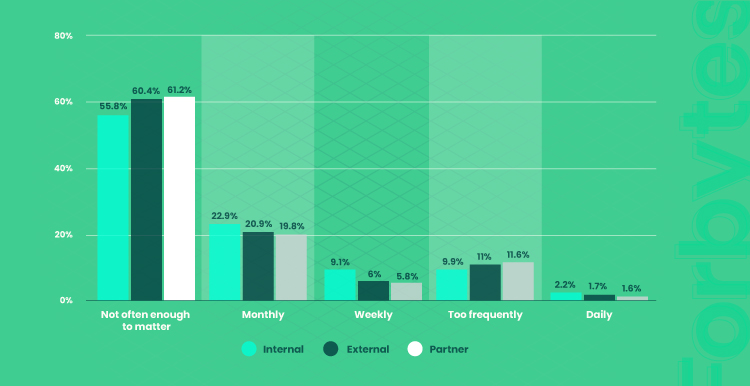

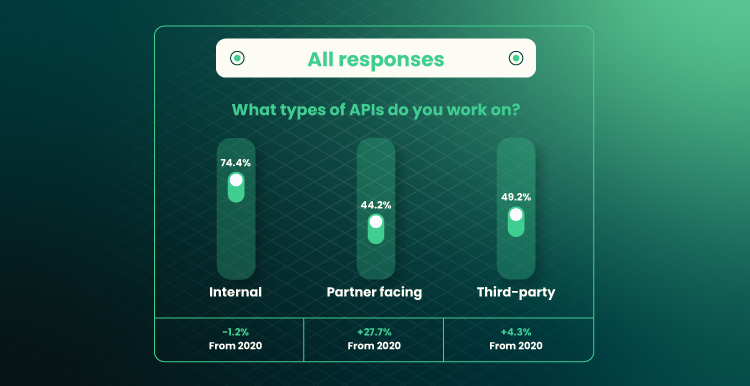

Experts persuade such clients that open interfaces are entirely secure. E.g., according to Statista, about 60% of entrepreneurs consider APIs safe. That’s confirmed by the chart above. Furthermore, under DEVELOPSdigest in 2021, nearly 49% of developers worked with third-party interfaces. It’s shown by the chart below.

Also, experts mention the World Fintech Report. According to it, about 89% of banks around the world used partner and open APIs within their business strategies in 2019. Thus, the mentioned trends show that third-party banking interfaces are completely safe for both financial institutions as well as customers. But it’s true only if experienced professionals implemented the system.

Main Advantages of Open Banking

Among the existing financial services, API stands out for its versatility. Such a digital interface suits both startups and large companies.

Nay, experts note the following key benefits of open banking APIs:

- Simplification of the procedure for obtaining or refinancing loans. Instead of collecting information from many sources and manually submitting it to potential lenders, consumers can let the creditors just take what they need and make a better offer.

- Ability to help developers expand the menu of custom functions. For example, they can create programs that give clients personalized financial projections. Furthermore, it’s possible to integrate software based on artificial intelligence. Such programs, e.g., may recommend the cheapest products consumers want.

- Facilitation of business lending. Creditors are sometimes willing to check the ledgers of potential clients if their small business needs a loan. Therefore, the customers have to produce reports that may be inaccurate by the time the lenders see them. The creditors can get all the necessary information from clients’ banks and accounting systems using open banking.

- Presence of great opportunities for improving banking services. Also, financial APIs help make the costs of these services lower. Additionally, open banking assists in making pricing more transparent.

- Ability to create simpler as well as cheaper accounting systems. It may give benefit to both businesses and consumers. For example, when customers send or obtain payments, the integrated systems can be updated immediately. As a result, clients may save time preparing their tax returns.

- Opportunity to create new payment methods. Transactions are an important component of the European open banking policy. And banks must allow third-party paying initiators to make payments on their behalf under PSD2. It’s not a new approach, but this method can make it easier for more service providers to process payments. And it leads to reducing payment processing costs and can also benefit businesses.

Moreover, open banking API integration increases the number of banking opportunities for businesses. When and how financial institutions can share personal data is specified by open banking programs. For example, clients from the UK have to agree to share information with certain partners. In contrast, in the USA, these are banks that currently manage (as well as regulate) how their customers share personal information (if the consumers agree with that). And such an approach limits user experience.

Standardization and Specification Within the API Development

Currently, programmers follow the general REST recommendations when creating the described financial interfaces. Such an approach makes it possible to offer different implementation options for APIs of the same type. And it entails spending time on the individual configuration of each interface.

This approach isn’t suitable, e.g., for developing APIs for state and large banks. In this case, the creation of a common technical standard is necessary. So far, these difficulties are being solved by applying the recommendations of large financial institutions as well as consortiums. And in the future, deeper standardization would help reduce entry barriers for fintech as well as other companies. Thus, nowadays, it’s better to contact specialists to integrate API.

Implementation of Public APIs in Bank Operations

Within bank integration, API requires pretty much time and qualified efforts. Skilled IT engineers commonly implement such digital concepts. The integration strategy may involve numerous and various steps. However, experts note the most important ones.

So, the strategy of open banking API implementation includes the following stages:

- Identifying a general purpose of the interface integration. There’re a few service domains (e.g., for finance tracking or making transactions). And the definition of the most suitable one would significantly decrease the fault risks within the company’s development.

- Preparation of a mechanism for both successful scaling of projects and quickly testing the hypotheses. Here, it’s necessary to combine research activities as well as select the most effective competitors’ methods. That’s because banks create various API sets, which may be accepted or rejected by the market. But, simultaneously, it required inventing something new to stay competitive.

- Clarification of initial purposes. At this stage, the impact of each open API on the financial institution should be assessed. Here, it may be necessary to consider the market share increase, the amount of additional income, geographic expansion, and so on.

- Separate the existing banking database information. Here, it’s needed to define client information for external and internal use. Additionally, it should be assessed whether the available data is suitable for training applications with artificial intelligence. Add-ons like these can help, e.g., identify fraudsters, investigate pricing patterns, or perform credit scoring.

- Preparation of a product development plan for each open banking API. Banks should make the necessary changes to the enterprise software architecture, prepare an information management system, fulfill checks for compliance with current regulations, etc.

- Selecting the right means for the project integration. E.g., financial institutions may use semi-finished solutions or create fully customizable APIs. But even the introduction of digital templates requires a great deal of professionalism. That’s why experts recommend contacting IT professionals to implement the projects’ part related to software development.

- Preparation for an API ecosystem creation. Collaboration with third parties helps banks increase the interest of existing customers, develop additional services to attract new consumers, and collect additional information about newcomers as well as permanent clients.

Open banking technology is constantly improving. Therefore, the above API integration strategy can be supplemented with new stages. Thus, experts recommend monitoring the current market trends to build an effective interface implementation plan.

The Future of Open APIs

Although banks and other financial institutions firstly were quite restrained in API banking, the benefits of such a digital interface are undeniable. The concept allows for making transactions quickly, freely, as well as safely. And such features are incredibly important for sellers, suppliers of payment services, and consumers.

Therefore, more and more banks, financial institutions, as well as fintechs integrate this technology into their corporate systems. Moreover, under CrustLab, the number of new API customers increased by 60% in 2022 compared to 2021 and amounted to 3.9 million users, along with 600,000 small enterprises. Furthermore, about 1 million clients join open banking every six months.

How to Select Proper Financial APIs for Implementation?

Not only European banks widely use open banking. The concept is also rapidly gaining popularity in Asia and North America. Therefore, the number of providers is growing swiftly. Additionally, fintechs and non-banking financial organizations also prepared some endpoints for third-party services integration. Developers have a wide range of opportunities for the implementation of open banking. But how should an entrepreneur choose the financial API for integration with a specific software product? Here are some recommendations from Forbytes specialists.

So, to choose the right banking API, the entrepreneurs should:

- Determine the strategic goal of implementation. It can be, for example, cross-sales, improving customer experience, or expanding the possibilities of detecting fraud.

- Select the most popular banks among customers. Then it’s needed to study which banking institutions are in demand within the target audience. It would help make a list of financial institutions for further analysis.

- Find and evaluate detailed documentation with frequently asked questions. Here, it should be considered that some open APIs can be paid. Furthermore, part of such interfaces has technical limits, e.g., the number of requests per hour.

- Analyze offers from various suppliers. It’ll help determine whether the problem would be solved by integrating a few APIs. E.g., if it’s needed to get the history of transactions to increase the efficiency of advertising campaigns, entrepreneurs have to check the availability of such services from a particular supplier.

- Check the security standards of the selected API for fintech. Here, it’s necessary to entrust the legal department to determine whether the data exchange process meets requirements. Also, lawyers have to develop a procedure for obtaining clients’ permits.

It’s also essential to plan several alternative ways to implement the project. It is because a detailed analysis may show that the selected suppliers don’t have the corresponding API. In this case, a business owner would have to find alternative APIs or other functions to solve the problem.

Conclusion

The concept of open banking today is, one way or another, used in most online services. Thus, business owners simply need to implement this technology to keep up with competitors. But when integrating an open banking API, it’s important to seek help from experienced IT specialists.

Contact us to get qualified advice on the described concept integration. Our agency team includes certified specialists with extensive experience in solving business problems within the IT field. In addition, the company offers an individual approach to each client as well as favorable prices.

Our Engineers

Can Help

Are you ready to discover all benefits of running a business in the digital era?

Our Engineers

Can Help

Are you ready to discover all benefits of running a business in the digital era?